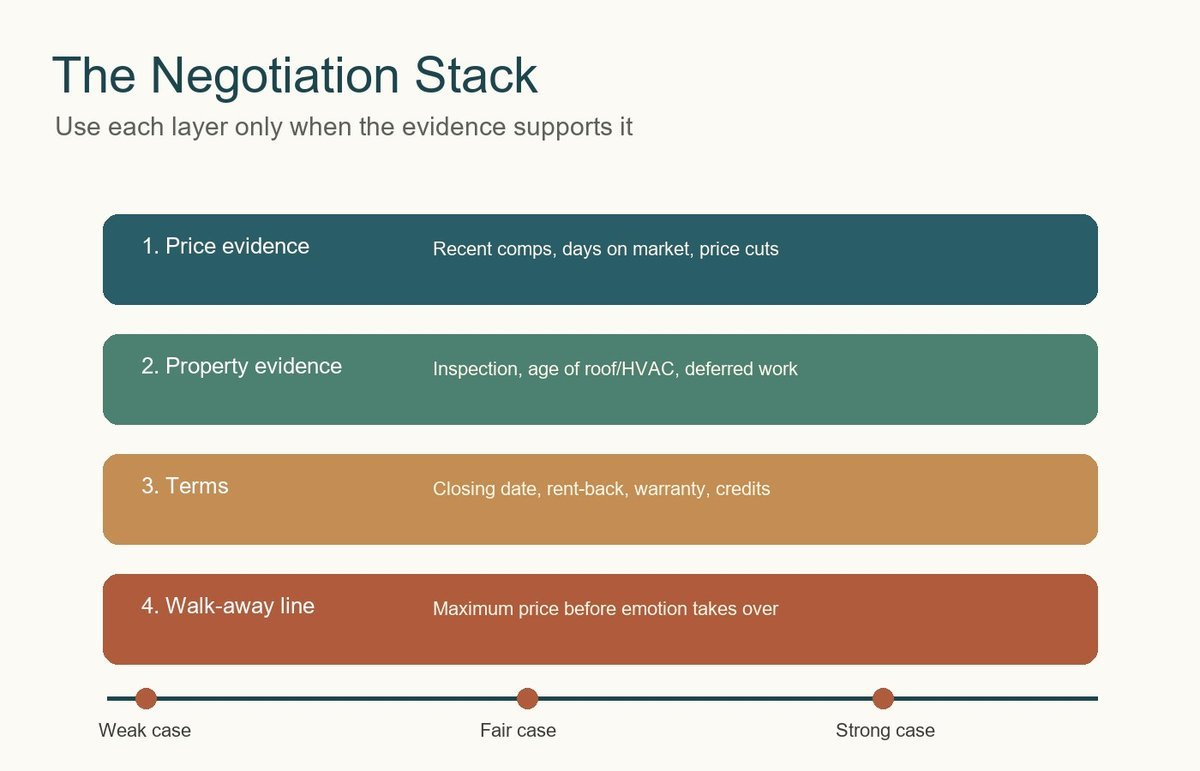

To negotiate on a house price, build your case around recent comparable sales, the home’s condition, the seller’s timeline, and the terms that make your offer easier to accept, explains TrueDoor Property Management professionals. The strongest buyers do not simply ask for a discount. They show why a lower price, closing credit, repair credit, or better closing timeline makes sense for that specific property.

Start With the Local Market, Not the Asking Price

The listing price is the seller’s opening position, not proof of value. Before asking for a lower price, compare the home with similar properties that recently sold in the same neighborhood, school zone, property type, age range, and condition bracket.

The simplest mistake is comparing a renovated home with an outdated one, or a larger lot with a smaller one. Your agent should pull recent closed sales first, then active listings, then pending sales if local MLS rules allow it. Closed sales show what buyers actually paid. Active listings show the seller’s competition. Pending sales, when available, hint at where demand is moving.

Use a clean three-column comparison:

| Evidence | What it tells you | How it helps negotiation |

|---|---|---|

| Recent closed comps | The most defensible range of market value | Supports a lower offer when the listing is above similar sales |

| Days on market | How long the seller has waited | Longer exposure may make a seller more open to concessions |

| Price reductions | Whether the seller has already adjusted expectations | Signals room to discuss price or credits |

| Condition differences | Repairs, age of systems, or outdated finishes | Turns emotion into a documented dollar conversation |

If the comps support the asking price, negotiation should shift away from a blunt discount and toward terms: seller-paid closing costs, a home warranty, a repair credit, appliances, timing, or a rate buydown contribution. If the comps do not support the price, your offer should explain the gap in plain numbers.

Set Your Walk-Away Number Before You Make the Offer

Your walk-away number is the maximum total cost you can accept after price, closing costs, repairs, taxes, insurance, and monthly payment are all counted together. Without that number, every counteroffer feels personal, and that is when buyers start paying for relief instead of value.

Write down three numbers before the first offer:

- Target price: the number that would make the home a strong buy based on comps.

- Fair price: the number that is acceptable if the seller gives useful terms.

- Walk-away price: the point where the home no longer fits your finances or risk tolerance.

The walk-away price should include monthly payment, cash to close, immediate repair exposure, and reserves after closing. A $5,000 price win does not help much if the roof, HVAC, or sewer line creates a $15,000 surprise three months later.

The Consumer Financial Protection Bureau reminds buyers that closing costs are not only lender charges. They can include title insurance, government taxes, appraisal fees, prepaid taxes, homeowners insurance, and interest. The CFPB also notes that seller credits are negotiable in some transactions, but they are not free money if the seller demands a higher price in exchange.

Make a First Offer That Leaves Room Without Insulting the Seller

A good first offer is low enough to protect your upside and reasonable enough to keep the seller engaged. The right discount depends on bargaining strength. A stale listing with two price cuts is different from a fresh listing with multiple showings in the first weekend.

As a practical starting point, use the market temperature:

| Situation | Likely approach | What to avoid |

|---|---|---|

| Multiple offers or low inventory | Offer close to asking, strengthen terms, protect key contingencies | A deep discount with no proof |

| Average demand and fair pricing | Offer modestly below asking with comp support | Overloading the offer with small demands |

| Long days on market or price cuts | Ask for a larger price adjustment or seller credit | Ignoring why the home has not sold |

| Visible repairs or outdated systems | Price the risk and leave room for inspection negotiation | Waiving inspection to win a small discount |

The offer should be simple enough for the seller to understand quickly. A useful framing sounds like this: “Based on three nearby sales between $482,000 and $497,000, plus the original HVAC system and roof age, our offer is $485,000 with standard inspection and financing contingencies.” That gives the seller something concrete to respond to.

Negotiate More Than the Purchase Price

The best deal is not always the lowest headline price. Cash to close, repair credits, closing date, contingencies, appliances, warranties, and seller-paid costs can change the real value of the transaction.

Buyers often focus only on the contract price because it is the easiest number to see. Sellers may care about a different problem: certainty, timing, fewer repairs before moving, or avoiding another month of carrying costs. That is where useful tradeoffs appear.

Consider these negotiable items:

- Seller credit toward closing costs: helpful when cash to close matters more than a slightly lower price.

- Repair credit: cleaner than asking the seller to complete rushed repairs before closing.

- Rate buydown contribution: useful when monthly payment is the pressure point.

- Home warranty: modest value, but sometimes useful for older appliances or systems.

- Closing date: powerful when the seller needs extra time or wants speed.

- Included property: appliances, window treatments, furniture, or outdoor equipment can matter.

Always check lender limits before relying on seller credits. Loan type, down payment, and occupancy can affect how much the seller is allowed to contribute. A credit that looks good in a counteroffer is useless if underwriting will not allow it.

Use the Inspection as a Second Negotiation, Not a Second Attack

The inspection is where negotiation becomes most legitimate because the conversation moves from opinion to condition. Focus on safety, structure, major systems, water intrusion, roof life, electrical issues, plumbing, pests, drainage, and anything likely to affect insurability or financing.

Do not nickel-and-dime the seller with every loose handle or paint scratch. Small complaints weaken the larger ask. Group inspection findings into three levels:

- Major deal items: roof, foundation, sewer, HVAC, electrical, mold, drainage, or structural concerns.

- Costly but manageable items: aging water heater, appliance failure, window issues, minor plumbing repairs.

- Cosmetic items: paint, worn carpet, small trim problems, ordinary wear.

Ask for a credit when possible, especially if the repair requires your own contractor choice after closing. A seller-completed repair can be fine, but the seller is naturally motivated to close the deal, not upgrade the property. If local rules, lender guidelines, or contract terms require the seller to repair something before closing, keep the request tightly written.

A strong inspection request might say: “The inspection found active plumbing leaks under the hall bath and a furnace at the end of expected service life. Buyer requests an $8,500 seller credit at closing in lieu of seller repairs.” That is specific, measurable, and easier to negotiate than a vague demand for the seller to “fix everything.”

Read Seller Motivation Without Guessing Too Much

Seller motivation matters, but it should be treated as context, not gossip. Useful signals include vacant homes, relocation language, estate sales, price reductions, long days on market, a failed previous contract, or a seller who needs a rent-back after closing.

Your agent can ask the listing agent direct but professional questions:

- Has the seller received other offers?

- Is there a preferred closing date?

- Would the seller value certainty over a higher price?

- Were there inspection or financing issues with any prior contract?

- Are there terms besides price that would help the seller choose an offer?

The answers shape your offer. A seller moving for a job may value speed. A seller who already bought another home may value certainty. A seller with heavy equity may be more flexible on credits than on public price reduction. A seller emotionally attached to the home may care about a clean, respectful offer more than a clever negotiation tactic.

Avoid the Mistakes That Make Sellers Stop Listening

House price negotiation fails when the buyer sounds unserious, underprepared, or impossible to close with. Sellers do not have to accept the highest offer if that offer looks risky. They also do not have to keep negotiating with a buyer who treats the process like a game.

Avoid these mistakes:

- Making a low offer with no evidence: “We just want a deal” is not a valuation argument.

- Changing demands repeatedly: too many new asks create doubt about whether you will close.

- Waiving protections blindly: a cheaper price can become expensive if you skip inspection or financing safeguards without understanding the risk.

- Overvaluing personal letters: they can raise fair housing concerns in some markets and should be handled carefully with professional advice.

- Ignoring monthly payment: price is not the whole cost when rates, taxes, insurance, HOA dues, and repairs are in play.

The cleanest buyer is not always the richest buyer. Preapproval, proof of funds, flexible timing, short response windows, and a calm repair strategy can make a slightly lower offer look better than a messy higher one.

How to Respond to a Counteroffer

A counteroffer is not a rejection. It is the seller showing the shape of a possible deal. Compare the counter with your target price, fair price, walk-away number, and the value of any terms the seller offered.

Use this decision rule:

- If the counter is inside your fair range, negotiate terms before pushing price again.

- If the counter is above your fair range but below your walk-away number, ask whether credits or repairs close the gap.

- If the counter is above your walk-away number, step back. A house that breaks the budget is not a win.

When you counter back, change only the points that matter. A buyer who counters price, closing date, repairs, appliances, and credits all at once can make the seller feel the deal will never settle. Pick the two or three items with real dollar value.

Sample Scripts for Negotiating a House Price

The best negotiation language is calm, specific, and tied to evidence. These examples can be adapted by your agent to match local practice and contract rules.

| Scenario | Useful wording |

|---|---|

| Comps support a lower price | “The closest recent sales support a range below the current list price, so the buyer is offering $X with standard contingencies.” |

| Inspection finds major repairs | “Based on the inspection findings and contractor estimate, buyer requests a $X credit at closing.” |

| Seller wants a fast closing | “Buyer can meet the preferred closing date if the seller can agree to $X or a $Y closing cost credit.” |

| Seller says price is firm | “If the seller cannot move on price, buyer would consider the current number with help on closing costs or specific repairs.” |

The Bottom Line

Learning how to negotiate on a house price is really learning how to turn uncertainty into a documented offer. The buyer who wins is not always the one who pushes hardest. It is often the one who knows the market, respects the seller’s constraints, protects their own budget, and asks for concessions that match the evidence.

If the home is fairly priced and competitive, negotiate with terms. If the home is overpriced, use comps. If the inspection reveals real defects, ask for a credit or repair solution. If the seller will not move and the numbers no longer work, walking away is not losing. It is the final negotiation tool that keeps one house from becoming a long financial regret.

FAQ

How much below asking price should I offer on a house?

The right amount below asking depends on comparable sales, local demand, days on market, property condition, and seller motivation. In a competitive market, a deep discount may fail quickly. On a stale or overpriced listing, a larger reduction can be reasonable when supported by comps.

Can I negotiate after the home inspection?

Yes, if your contract includes an inspection contingency or local practice allows repair negotiations. Focus on major safety, structural, system, water, pest, or insurance-related issues. A clear repair credit request is usually stronger than a long list of minor complaints.

Is it better to ask for a lower price or seller-paid closing costs?

A lower price reduces the loan amount, while seller-paid closing costs can reduce cash needed at closing. The better choice depends on your cash position, lender rules, appraisal risk, and monthly payment. Ask your lender how credits affect your loan before making them central to the offer.

Should I negotiate directly with the seller?

Most buyers should negotiate through their real estate agent or attorney, depending on local practice. Direct emotional conversations can create misunderstandings. A professional can keep the message factual, documented, and aligned with contract deadlines.

When should I stop negotiating?

Stop when the seller’s price and terms exceed your walk-away number, when inspection risk becomes too large, or when the deal requires you to waive protections you do not understand. The goal is not to win the argument. The goal is to buy the right house at a price and risk level you can live with.

What Buyer Forums Reveal About Negotiation Anxiety

Real buyer discussions show that most negotiation stress comes from uncertainty, not greed. Buyers are usually trying to understand whether a lower offer is reasonable, whether an agent is pushing them too hard, or whether inspection problems justify a second ask.

On r/FirstTimeHomeBuyer, a community focused on the messy first purchase, one buyer captured the emotional bind perfectly: they wanted to start low on a $250,000 listing, but their agent kept warning that the house would probably go higher than list.

“I’m buying a house for the first time… my realtor is not inclined to doing that. Can someone explain why.”

— r/FirstTimeHomeBuyer, April 2026 (0 upvotes)

That is the human part of negotiation most checklists miss. A buyer is not only calculating price. They are wondering whether their agent is protecting them, whether the seller will be offended, and whether they will look naive for asking. The answer is not to stop negotiating. It is to make the offer defensible enough that the conversation stays about the house, not the buyer’s nerve. That is the quiet skill behind how to negotiate on a house price well.

Inspection anxiety has the same pattern. In a HousingUK thread about a 15-year-old boiler, the buyer said the choices felt overwhelming and wondered whether to push for a credit or simply plan for the replacement. The replies were split, which is exactly why inspection negotiation needs judgment.

“Expect the seller to tell you to jog on.”

— r/HousingUK, April 2026 (73 upvotes)

Another commenter argued that if the boiler still works and is safe, asking for money off may be weak. That disagreement is useful. It shows why the strongest inspection request is not “this is old, so pay me.” It is “this defect changes the cost or risk of ownership, and here is the estimate.”

- A buyer thread about being told the seller’s price is firm

- A buyer thread about negotiating after roof issues appear in inspection

Sources

- National Association of Realtors existing-home sales data

- NAR 2025 Profile of Home Buyers and Sellers newsroom release

- CFPB explanation of mortgage closing costs and seller credits

- CFPB Loan Estimate and Closing Disclosure guide